Automating Complex Tasks in Portfolio Management: How AI and Technology Are Transforming Advisor Efficiency

Table of contents

The wealth management industry is at a clear automation tipping point:

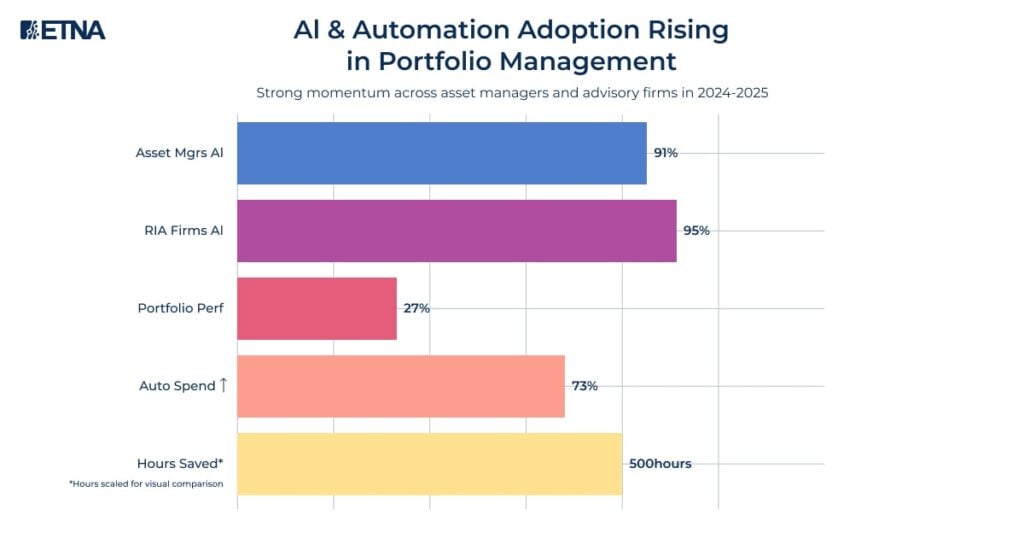

Roughly 9 in 10 asset managers report that they are already using or actively planning to use AI in their portfolio management workflows, spanning from idea generation to risk monitoring.

RIA and wealth firms that adopt AI and workflow automation report double‑digit improvements in portfolio performance, client satisfaction, and practice profitability, while reducing operational overhead.

Advisors who utilize automation at scale typically recover hundreds of hours per year, which can be redeployed into planning, client meetings, and business development, rather than manual trading and reporting.

For modern advisory firms, especially RIAs and hybrid practices, the core levers are:

Automatic diversification (AI‑ and rules‑driven portfolio construction).

Automated portfolio rebalancing (always-on drift control + tax optimization).

Hands‑off investing experiences for clients that still sit on a compliant advice platform.

Automated withdrawal schedules that turn portfolios into predictable retirement paychecks.

These automation pillars are precisely where platforms like ETNA’s RIA solution are focusing their product roadmap, combining advanced trading infrastructure with advisor-friendly oversight.

The Automation Imperative: Why Portfolio Management Technology Matters Now

Manual portfolio management simply doesn’t scale to modern client expectations and regulatory complexity:

Advisors must manage multi‑asset portfolios, multi‑custodian data feeds, tax‑aware transitions, and evolving compliance requirements, all while delivering more digital self‑service and real‑time transparency to clients.

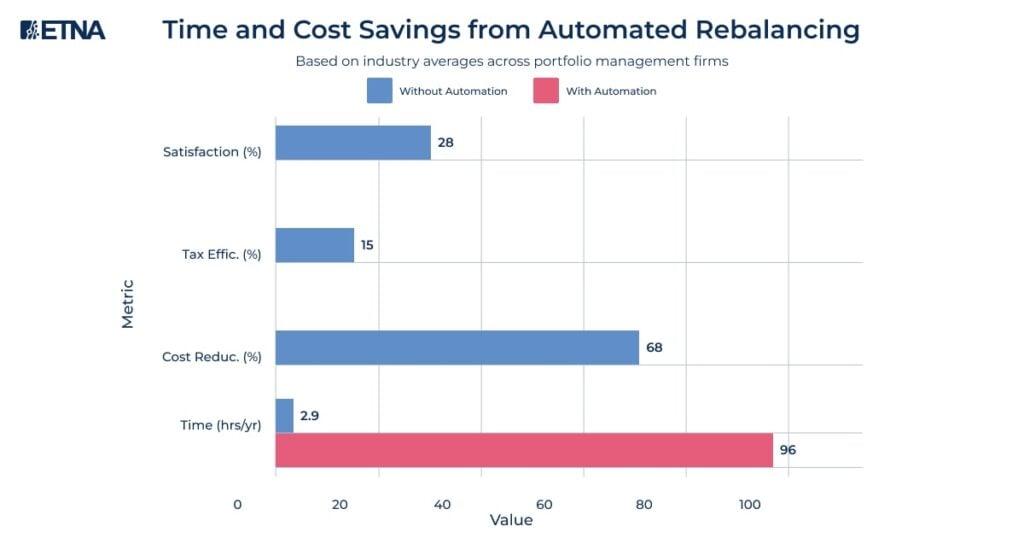

Industry automation indexes show more than 70% of companies increased automation spending in 2025, with a material subset reporting 25–50% reductions in process costs after implementation.

In the RIA segment, technology and portfolio management market studies consistently describe a large adoption gap: thousands of firms still rely on spreadsheets and manual trade files despite the availability of mature automation platforms.

For advisors, the automation business case boils down to three outcomes:

Time leverage

Routine tasks like rebalancing, cash sweeps, and model updates move from hours to minutes per household.

Advisors reallocate saved time toward planning conversations, complex cases, and prospecting.

Risk and compliance control

Automated rules enforce trading permissions, pattern day trading guardrails, household suitability, and model drift limits in real time.

Every rebalance and exception can be logged for auditability and supervisory review.

Scalable client experience

Clients get institutional‑grade portfolio construction, always‑on monitoring, and mobile access without requiring advisor “heroics” behind the scenes.

Automatic Diversification: Building the Best Diversified Portfolio Through Technology

Automatic diversification is where the “best diversified portfolio” theory meets modern infrastructure.

What’s changing:

Algorithms and models do the heavy lifting

Portfolio engines apply modern portfolio theory, factor models, and risk budgeting at scale to design target allocations that balance growth, income, and downside protection.

AI‑enhanced engines incorporate additional signals (factor tilts, volatility regimes, sentiment, macro inputs) that would overwhelm manual workflows.

True multi‑dimensional diversification

Across asset classes: equities, fixed income, cash, real estate, commodities, and alternatives.

Across geographies and sectors to avoid home‑country and single‑industry concentration risk.

Across styles and factors (growth vs. value, quality, low volatility, momentum).

Client and advisor benefits:

Automatic diversification keeps portfolios aligned with risk profiles without requiring an advisor to hand‑craft each allocation.

Automated engines can push clients toward a best diversified portfolio given their constraints, while still allowing advisors to add guardrails (ESG filters, security bans, legacy holdings).

The process is repeatable and explainable advisors can show clients exactly how their diversification reduces volatility and improves risk‑adjusted returns over time.

For advisory firms:

Automatic diversification serves as the “model factory” behind model portfolios and risk‑based sleeves that can be assigned across hundreds or thousands of accounts with a consistent, documented methodology.

Advanced rebalancing algorithms keep each household aligned with its investment objectives, adjusting allocations based on predefined models and live market movements.

Advisors can:

Build model portfolios by asset class, risk tolerance, or investment themes (e.g., income, growth, ESG).

Combine or nest models for more sophisticated allocation plans (core‑satellite, UMA‑style setups).

This lets RIAs automate the mechanics of rebalancing while retaining policy control and the ability to override or queue trades at the advisor level.

Hands-Off Investing for Advisors: Enabling Passive Strategies at Scale

Hands‑off investing marries automated portfolios with advisor oversight:

Clients get a largely “autopilot” experience:

Automated account funding, recurring investments, drift control, and tax‑loss harvesting.

Mobile and web dashboards that explain allocation, performance, and risk in plain language.

Advisors maintain control of:

Model design and selection.

Suitability, risk profile alignment, and household‑level exceptions.

Key dynamics in today’s market:

Robo‑advisors and digital advice platforms continue to grow assets under management thanks to low fees, easy onboarding, and always‑on automation.

Hybrid models (automation + human advisor) consistently achieve higher satisfaction and retention than stand‑alone digital or stand‑alone human approaches.

Benefits for advisory firms:

Scalable service tiers

Entry‑level, hands‑off “digital first” offers for smaller accounts and accumulators.

Higher‑touch planning for HNW clients, with the same automation engine running the portfolio in the background.

Behavioral coaching margin

Because the heavy lifting of trading and monitoring is automated, advisors have more bandwidth to coach clients through volatility, life events, and decision points where human value is highest.

ETNA supports this through:

A white‑label robo‑advisor stack and a dedicated RIA platform with automated model portfolios, digital onboarding, and client self‑service.

Three delivery modes robo, hybrid, and full‑service advisory on the same infrastructure, so firms can mix hands‑off investing with bespoke advice as needed.

Automated Withdrawal Schedules: Retirement Income Planning Simplified

Once clients enter the decumulation phase, automation shifts from accumulation to systematic withdrawals:

What automated withdrawal schedules do:

Turn account balances into predictable, rules‑based income streams (monthly, quarterly, or annual draws).

Coordinate withdrawals across account types (taxable, tax‑deferred, Roth) using pre‑defined tax and sequencing rules.

Track and help satisfy required minimum distributions (RMDs) without manual calculations.

Industry data points:

A growing share of 401(k)/DC plans now include in‑plan systematic withdrawal options, but demand still significantly outstrips supply participants want predictable income and automation, not one‑off lump sum decisions.

Advisor and client benefits:

For clients:

“Paycheck‑like” retirement income that doesn’t require constant calls or manual transfers.

Reduced risk of overspending or underspending relative to plan assumptions.

For advisors:

Less operational friction in processing distributions across dozens or hundreds of retiree households.

Easier monitoring of cash flow sustainability and faster identification of accounts that need plan adjustments.

How ETNA fits:

ETNA’s RIA platform supports automated, rules‑based withdrawal workflows that can be integrated with its rebalancing and portfolio management engines, so income, risk, and allocation stay in sync instead of being managed in silos.

AI and Machine Learning: The Next Frontier in Portfolio Management

AI and machine learning are moving beyond rule‑based automation to predictive, adaptive portfolio management:

91% of asset managers are using or planning AI; institutional investors see ~27% better performance.

The global AI in asset management market is projected to grow from $4.6B (2024) to $38.9B (2034).

Key AI applications:

Algorithmic trading: Execute trades at optimal prices with speed and precision.

Predictive analytics: Forecast market moves and identify emerging risks.

Sentiment analysis: Gauge market psychology from news, social media, and filings.

Natural language processing: Extract insights from unstructured data (reports, transcripts, etc.).

AI also enables hyper‑personalization at scale:

Analyze client behavior, risk tolerance, and life events to generate tailored strategies.

Enhance engagement and satisfaction while serving more clients.

For advisors, AI integration delivers:

Higher returns: AI‑powered tools outperformed traditional methods by ~14% in 2025.

Lower costs: ~30% cost savings and ~80% workload reduction in some implementations.

Better risk management: Continuous monitoring of concentrations, correlations, and early‑warning signals.

Implementation Best Practices: Choosing and Deploying Automation Technologies

To implement automation successfully, focus on:

1. Integration & connectivity

Choose platforms that integrate natively with custodians, CRMs, and financial planning tools.

Prioritize robust APIs and cloud‑based solutions for scalability and remote access.

2. Automation sophistication

Look for advanced rebalancing engines that handle complex restrictions, tax sensitivity, and multi‑asset classes.

95% of RIAs already use AI tools; 91% of asset managers are actively adopting AI.

For advisors, the choice is straightforward:

Embrace automation to free hundreds of hours, serve more clients, and deliver better outcomes.

Or risk falling behind as early adopters build insurmountable advantages.

ETNA’s platform delivers the integrated automation advisors need:

Automated RIA product portfolio rebalancing.

Automated withdrawal schedule features.

Multi‑custodian integration, dual‑license support, and strong compliance tools.

The future belongs to advisors who combine the power of technology with human judgment, empathy, and relationship skills. By automating complex tasks, advisors can focus on what matters most: helping clients achieve their financial goals.

Ask us anything about platforms, integrations, or business growth.

We use cookies and similar technologies that are necessary to run our website. By clicking “Accept,” you agree to our Cookie policy and Privacy policy.